Setting Up Your Chart of Accounts

Step-by-step guide to creating and organizing a chart of accounts for your business. Learn which accounts you need and how to structure them.

Read MoreMaster the fundamental rule that powers double-entry bookkeeping. Every debit and credit you’ll ever record follows this core principle.

You’ve probably heard these terms thrown around if you’re new to accounting. Thing is, they’re not complicated once you understand the basic concept. Debits and credits aren’t mysterious — they’re just a way of recording which direction money or value moves in a transaction.

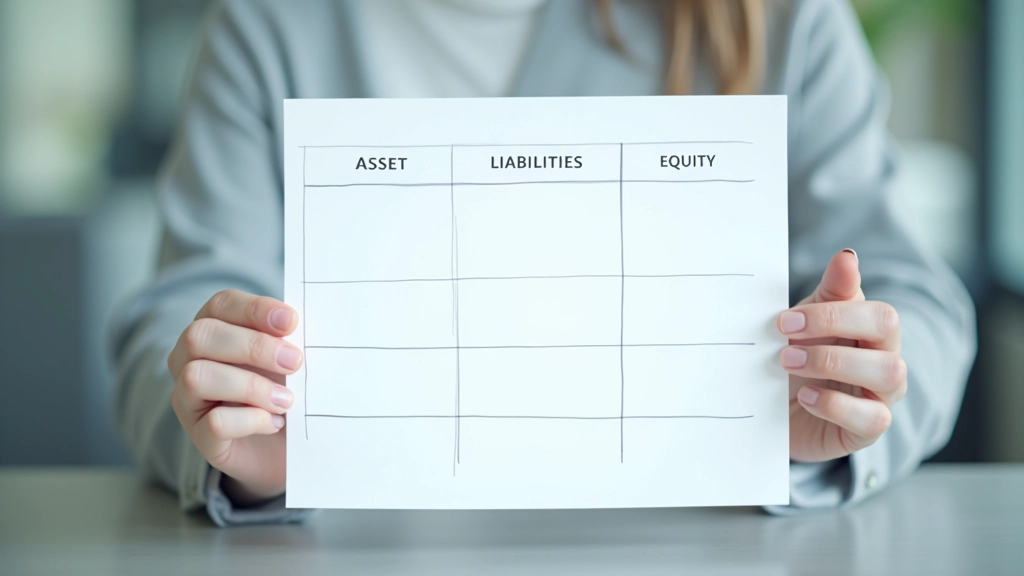

In double-entry bookkeeping, every transaction affects at least two accounts. One account gets debited, another gets credited. This creates balance. It’s the reason the accounting equation (Assets = Liabilities + Equity) always stays balanced. We’ll walk you through how this works so it actually makes sense.

This single principle determines how every transaction gets recorded

Debit entries appear on the left side of an account. They increase asset accounts and expense accounts. They decrease liability accounts, equity accounts, and revenue accounts.

Credit entries appear on the right side. They do the opposite of debits. Credits increase liabilities, equity, and revenue. They decrease assets and expenses.

Total debits must equal total credits. Always. This balance is what makes double-entry bookkeeping work. It’s your built-in error check.

The direction changes depending on what type of account you’re dealing with. Assets, liabilities, equity, revenue, and expenses all behave differently. Here’s what you need to remember:

Debits increase, credits decrease. When you buy equipment, you debit the equipment account. When you sell it, you credit the account.

Credits increase, debits decrease. You owe money? That’s a credit balance. When you pay down debt, you debit the liability account.

Credits increase owner’s equity, debits decrease it. Your investment goes in as a credit. Withdrawals are debits.

Credits increase revenue, debits decrease it. When you make a sale, you credit the revenue account. This seems backward until you remember that revenue increases equity.

Debits increase expenses, credits decrease them. You spend money on rent? Debit the rent expense. This makes sense because expenses reduce profit.

Let’s say your business receives RM5,000 in cash from a customer. You’d record this in two accounts:

Cash is an asset. Assets increase with debits.

Revenue increases with credits. The totals balance.

Notice how the debit equals the credit? That’s the double-entry system working. Both sides of the equation stay balanced. Your total debits recorded today must equal your total credits. If they don’t, you’ve made an error somewhere.

Most accountants develop mental shortcuts after a while. Here are some that actually work:

Visualize each account as a T. The left side is debit, the right is credit. This simple shape helps you remember which side is which when you’re confused.

Assets are what your business owns. They increase with debits and decrease with credits. It’s straightforward — more stuff means a debit.

Liabilities are what you owe. They work opposite to assets. Credits increase liabilities, debits decrease them. Owing more money? That’s a credit.

Assets = Liabilities + Equity. Keep this balanced. Every transaction affects this equation on both sides, which is why debits must equal credits.

In every transaction, debits must equal credits. This is the foundation of double-entry bookkeeping. It’s not optional — it’s the rule.

The same transaction direction (debit or credit) doesn’t work for every account. Assets increase with debits, but liabilities increase with credits. Know your account types.

Assets = Liabilities + Equity. Every debit and credit you record maintains this balance. If your books don’t balance, you’ve made a mistake. This is your quality control.

The first few transactions might feel confusing. But after recording 20 or 30 entries, you’ll stop thinking about which side goes where. It becomes automatic.

This article provides foundational information about debit and credit concepts in double-entry bookkeeping. It’s designed to help you understand basic accounting principles. For specific accounting guidance related to your business or tax situation in Malaysia, consult with a qualified accountant or tax professional who understands your circumstances. Accounting rules and tax requirements vary by business type and situation. The examples shown here are simplified for learning purposes.